Private Equity groups are often designed to target firms doing $5M+ in EBITDA, leaving great cash-flowing companies to be overlooked and trade in a highly inefficient lower micro-market.

Sundial targets B2B firms that provide essential products or services with 10+ years in business. We're industry agnostic, but it must be boring and growing.

The company should be doing $3M+ in Sales, $1-4M in EBITDA, have strong customer concentration dispersion (<20% from top 20 customers), and have little to no marketing team.

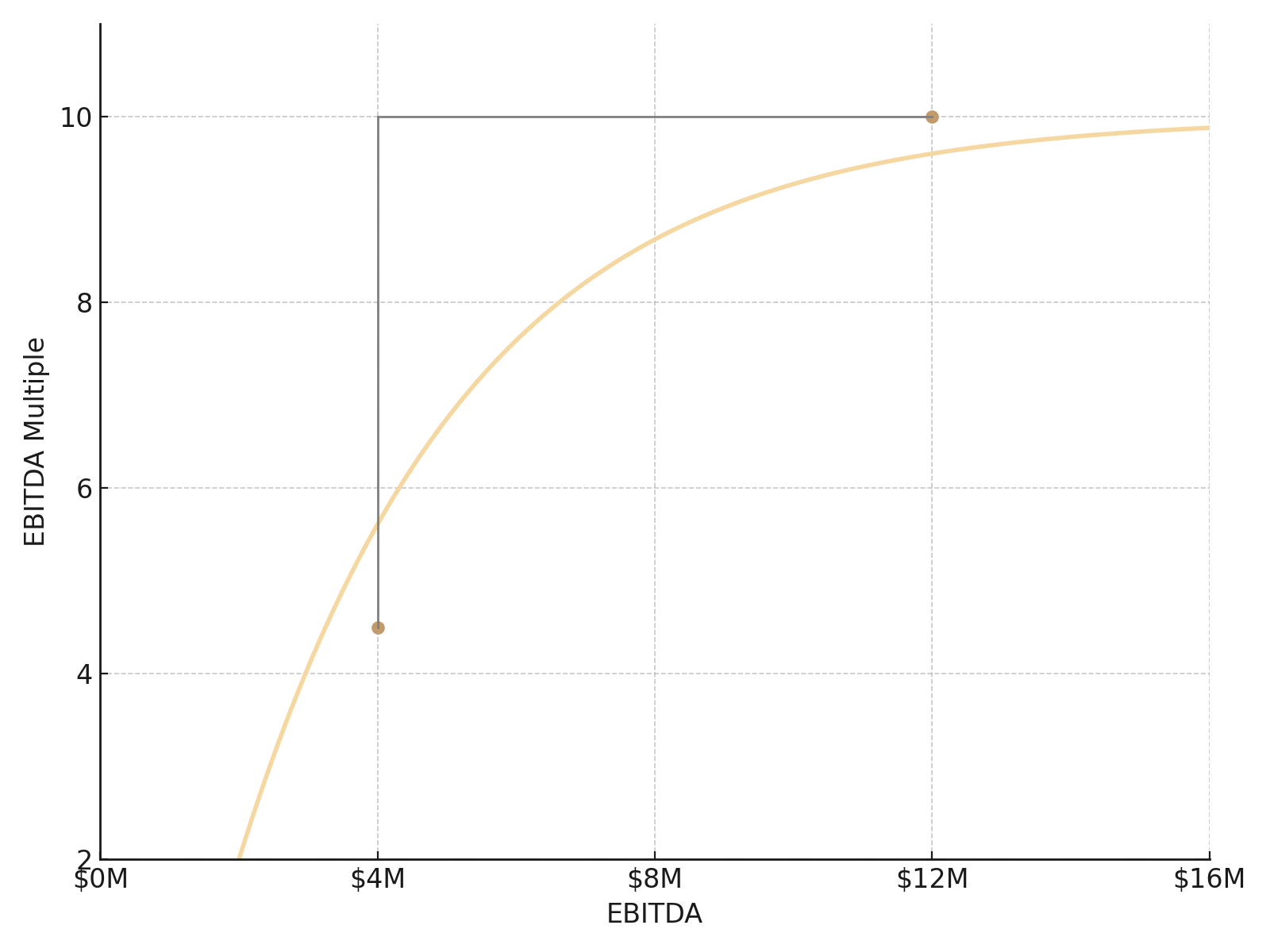

The steepest part of the valuation curvetakes place when a firm grows from $4M to $12M in EBITDA.

Sundial scales firms through this curve through organic growth + bolt-on acquisitions.

Sundial builds firms to last forever. But in the event of a sale, the valuation increase generates 5X+ MOIC.

Sundial distributes the excess cash flows on a quarterly basis back to Member Families, targeting 20%+ cash-on-cash annual yields.

.png)